Two aluminium smelters in the Gulf have reduced production within days of each other.

Two aluminium smelters in the Gulf have reduced production within days of each other.

That should make the aluminium market pay attention.

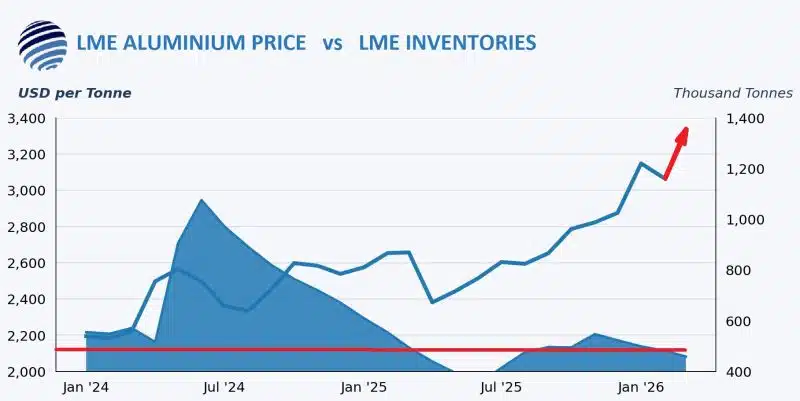

In our previous post we discussed the unusual combination of rising aluminium prices and declining LME inventories. Since then, another development has emerged that is worth watching.

First reports indicated that Qatalum reduced production. Now Aluminium Bahrain (Alba) has reportedly initiated a controlled shutdown of Reduction Lines 1–3, representing roughly 19% of its production capacity.

This does not appear to be a technical issue, but rather a precautionary response to uncertainty around logistics and raw material flows. Much of the discussion around the Strait of Hormuz focuses on oil and gas. But for the aluminium industry this corridor is equally critical.

The Gulf region has become one of the world’s key aluminium export hubs. Producers such as Emirates Global Aluminium, Aluminium Bahrain, Ma’aden and Qatalum together ship roughly 6 million tonnes of aluminium per year, which is approx. 10% of global primary aluminium production. Unlike oil, aluminium has no pipeline alternative.

It moves as ingots, billets and slabs…by ship.

When uncertainty affects a corridor like Hormuz, producers typically respond cautiously:

• slowing production where necessary

• protecting raw material inventories

• prioritising operational stability

Which appears consistent with what we are seeing now.

One aspect often overlooked is how aluminium smelters operate. Primary aluminium production is a continuous electro-chemical process. Potlines cannot simply be switched off and on again. Once production is reduced, restarting capacity requires stabilising the process, securing raw materials and ensuring reliable energy supply. In practice, bringing capacity back online happens gradually and can take weeks or even months before a smelter returns to normal output.

For the market this has two implications.

--> In the short term, announcements like these often increase volatility. Buyers and traders may move earlier to secure material, supporting LME prices and strengthening physical premiums.

--> In the longer term, the key question is whether these adjustments remain temporary or evolve into broader supply constraints across the region.

If shipping routes stabilise and raw material flows normalise, production can usually be restored step by step and markets tend to rebalance relatively quickly.

However, if uncertainty around logistics or energy persists, the aluminium market could remain tighter for longer than expected.

Europe imports roughly 1.2–1.4 million tonnes of primary aluminium from the Middle East each year, representing a meaningful share of regional supply.

European markets are already seeing the first effects through rising LME prices and stronger regional premiums. If disruptions in the Gulf expand further, the next stage could be tighter physical availability as well.

How do you see this developing?